03 — Inside the spreadsheet

Every check ends at $0.

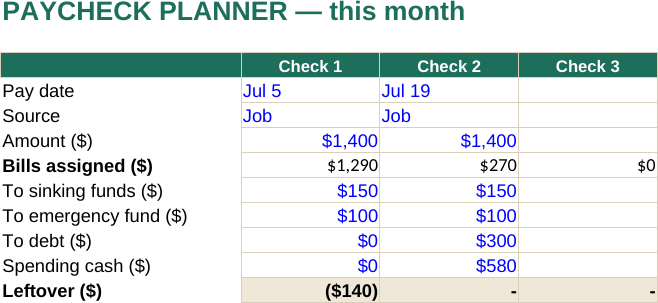

Enter a paycheck. The Planner shows the bills it carries, what's left, and where the leftover goes. Decided on payday, not discovered at month-end.

- Income Log — finds your lowest month for you

- Paycheck Planner — zero-based, per check

- Bills Calendar · Sinking Funds · Debt Snowball · weekly Dashboard